单选题

编号:2695696

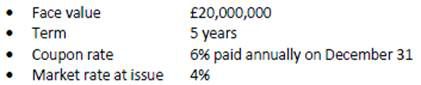

1. On 1 January 2009, a company that prepares its financial statements according to IFRS issued bonds with the following features:

The company did not elect to carry the bonds at fair value. In December 2011 the market rate on similar bonds had increased to 5% and the company decided to buy back (retire) the bonds after the coupon payment on December 31. As a result, the gain on retirement reported on the 2011 statement of income is closest to:

The company did not elect to carry the bonds at fair value. In December 2011 the market rate on similar bonds had increased to 5% and the company decided to buy back (retire) the bonds after the coupon payment on December 31. As a result, the gain on retirement reported on the 2011 statement of income is closest to: