单选题

编号:2695444

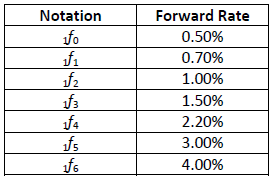

1. Assume the following six-month forward rates (presented on an annualized, bond-equivalent basis) were calculated from the yield curve.

The 3-year spot rate is closest to:

The 3-year spot rate is closest to: