单选题

编号:2692397

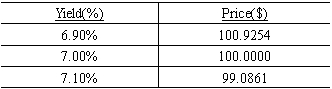

1. The table below summarizes the yields and corresponding price for a hypothetical 15-year option-free bond that is initially priced to sell at 7% yield:

Using a 10 basis point rate shock, the effective duration for this bond closest to:

Using a 10 basis point rate shock, the effective duration for this bond closest to: